EMI Affordability Rule: How Much EMI Should You Pay?

MBA Finance | CFA | Ex-Banker

Published March 23, 2026

EMI Affordability Rule: How Much EMI Should You Pay?

Taking a loan has become a common part of modern life. Whether it is for buying a home, a car, or managing personal expenses, loans help people achieve their financial goals faster. However, one of the biggest mistakes many borrowers make is not understanding how much EMI they can actually afford.

Choosing the wrong EMI amount can lead to financial stress, missed payments, and long-term financial problems. This is why it is very important to follow an EMI affordability rule before taking any loan.

In this detailed guide, we will explain how much EMI you should pay, how to calculate it based on your income, and tips to manage your loan smartly.

What is EMI Affordability?

EMI affordability refers to the amount of monthly installment you can comfortably pay without affecting your daily expenses, savings, and lifestyle.

It is not just about whether you can pay the EMI, but whether you can pay it consistently without financial pressure.

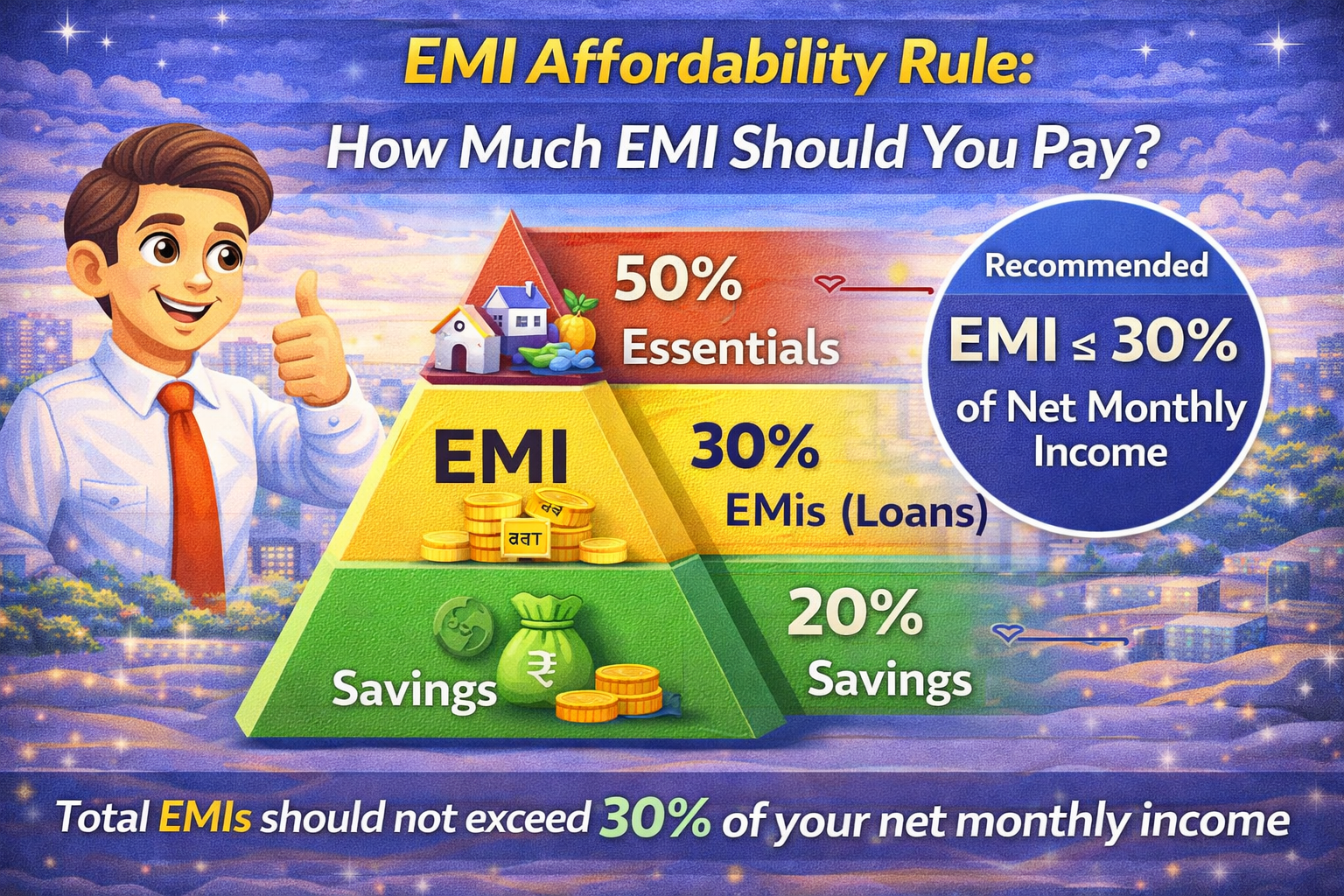

The 30% to 40% EMI Rule

Financial experts suggest that your total EMI should not exceed 30% to 40% of your monthly income.

For example, if your monthly income is ₹50,000, your EMI should ideally be between ₹15,000 to ₹20,000.

This ensures that you have enough money left for other expenses like rent, groceries, bills, savings, and emergencies.

EMI Based on Income Example

| Monthly Income | Safe EMI (30%) | Max EMI (40%) |

|---|---|---|

| ₹30,000 | ₹9,000 | ₹12,000 |

| ₹50,000 | ₹15,000 | ₹20,000 |

| ₹1,00,000 | ₹30,000 | ₹40,000 |

Why EMI Planning is Important

Proper EMI planning helps you avoid financial stress and ensures that you can manage your loan comfortably. If your EMI is too high, it can affect your savings and lifestyle.

On the other hand, if your EMI is too low due to long tenure, you may end up paying more interest.

Factors That Affect EMI Affordability

There are several factors that determine how much EMI you can afford.

Your monthly income is the most important factor. Higher income allows higher EMI.

Existing loans also affect your EMI capacity. If you already have EMIs, your affordability reduces.

Your lifestyle and expenses also play a key role. Higher expenses mean lower EMI capacity.

Interest rate and loan tenure also impact EMI amount.

Common Mistakes to Avoid

Many borrowers take loans based on maximum eligibility instead of affordability.

Ignoring future expenses is another common mistake.

Not keeping an emergency fund can create problems during unexpected situations.

Smart Tips to Manage EMI

Always calculate EMI before taking a loan.

Choose a loan tenure that balances EMI and interest.

Avoid taking multiple loans.

Increase EMI when your income increases.

Make prepayments whenever possible.

Real Life Scenario

Suppose your monthly income is ₹60,000. According to the 30% rule, your EMI should be around ₹18,000. If you take a loan with EMI ₹30,000, it may be difficult to manage your expenses.

This shows the importance of choosing the right EMI amount.

Long-Term Financial Stability

EMI is a long-term commitment. Proper planning ensures that you can manage it without stress.

Always plan your EMI based on current income and future goals.

Conclusion

Choosing the right EMI amount is very important for financial stability. By following the 30% to 40% rule and planning carefully, you can manage your loan easily.

Financial Tip: Never choose EMI based on loan eligibility. Always choose EMI based on your comfort and financial capacity.

About the Author

Admin

MBA Finance | CFA | Ex-Banker

Financial expert with 15+ years of experience in banking and personal finance.