How Loan Tenure Impacts Your EMI and Total Interest

MBA Finance | CFA | Ex-Banker

Published March 20, 2026

When taking a loan, most people focus only on the EMI amount. They try to choose the lowest EMI possible so that their monthly budget is not disturbed. However, what many borrowers fail to understand is that EMI is directly connected to loan tenure, and this decision can significantly impact the total interest you pay over time.

Loan tenure refers to the total duration over which you repay your loan. It can range from a few months to several years depending on the type of loan. While a longer tenure reduces your EMI, it increases the overall interest paid. On the other hand, a shorter tenure increases your EMI but reduces the total cost of the loan.

Understanding how tenure works is very important for making smart financial decisions. It is not just about choosing a lower EMI, but about balancing affordability with long-term savings.

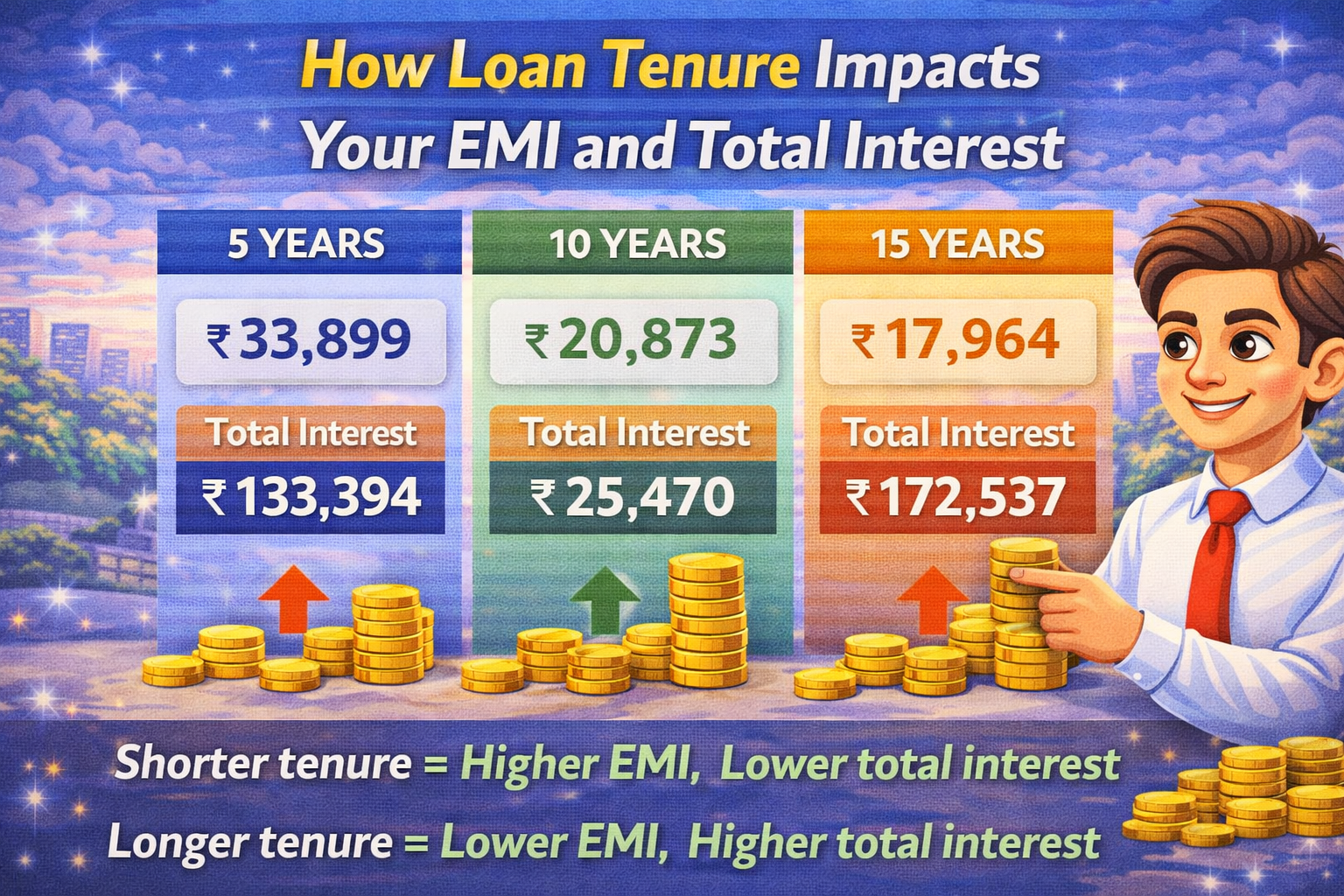

Let us understand this with a simple example. Suppose you take a loan of Rs. 10,00,000 at an interest rate of 10 percent per year. If you choose a tenure of 5 years, your EMI will be higher compared to a 10-year loan. However, the total interest paid in 5 years will be much lower.

If you choose a 10-year tenure, your EMI becomes more manageable, but you will end up paying a significantly higher amount in interest. This is because interest keeps accumulating over time.

This is why choosing the right tenure is very important. It should be based on your income, expenses, and long-term financial goals.

Many people prefer longer tenure because it gives them flexibility. Lower EMI means less pressure on monthly income. This is especially helpful for individuals who have multiple financial responsibilities such as household expenses, children’s education, or other loans.

However, the downside of longer tenure is the increased total interest. Over a long period, even a small interest rate can result in a large amount of extra payment.

On the other hand, shorter tenure is ideal for people who have stable income and can afford higher EMI. It helps in closing the loan faster and saving money on interest. This option is beneficial for those who want to become debt-free quickly.

Another important factor to consider is income growth. If you expect your income to increase in the future, you can start with a moderate EMI and gradually increase your payments through prepayment. This helps reduce tenure and total interest.

Prepayment is one of the best ways to manage your loan efficiently. Whenever you have extra funds, you can use them to reduce your principal amount. This directly reduces both EMI burden and interest cost.

Many banks allow partial prepayment without heavy charges, especially for floating rate loans. It is always a good idea to check these terms before taking a loan.

Another strategy is to use an EMI calculator before finalizing your loan. This tool helps you understand how different tenure options affect your EMI and total interest. It allows you to compare scenarios and choose the best option.

For example, you can calculate EMI for 5 years, 7 years, and 10 years, and see how much extra interest you are paying in each case. This gives a clear picture and helps you make informed decisions.

It is also important to consider inflation and future expenses. While a longer tenure may seem comfortable today, it can become a burden in the future if your expenses increase.

Similarly, choosing a very short tenure without proper planning can lead to financial stress. High EMI can disturb your monthly budget and reduce your ability to save or invest.

The key is to maintain balance. Your EMI should be affordable while also keeping total interest under control. Financial experts often suggest that your EMI should not exceed 30 to 40 percent of your monthly income.

This ensures that you have enough money for other expenses and savings.

Another important aspect is loan type. Different loans have different tenure options. For example, home loans usually have longer tenure compared to personal loans. Choosing the right tenure depends on the purpose of the loan.

You should also consider your risk appetite. If you prefer stability, shorter tenure is better. If you need flexibility, longer tenure may suit you.

In conclusion, loan tenure is not just a number. It is a critical factor that affects your financial health. Choosing the right tenure can help you save money, reduce stress, and achieve your financial goals.

Always analyze your income, expenses, and future plans before deciding. Use tools like EMI calculators and consult financial experts if needed.

A smart decision today can save you a lot of money in the future.

About the Author

Admin

MBA Finance | CFA | Ex-Banker

Financial expert with 15+ years of experience in banking and personal finance.